Comparing Robo Advisors vs Traditional Financial Advisors

A detailed comparison of robo-advisors and traditional financial advisors to help you choose the best investment guidance.

A detailed comparison of robo-advisors and traditional financial advisors to help you choose the best investment guidance.

Comparing Robo Advisors vs Traditional Financial Advisors

Hey there, future investor! So, you're looking to get your money working for you, which is awesome. But then you hit a fork in the road: do you go with a fancy new robo-advisor or stick with a good old traditional financial advisor? It's a common dilemma, especially for folks in the US and Southeast Asia, where both options are becoming super popular. Let's break down everything you need to know to make the best choice for your financial journey.

Think of it this way: a robo-advisor is like a super-smart, automated investment assistant. You tell it your goals, your risk tolerance, and it builds and manages a portfolio for you using algorithms. Traditional advisors, on the other hand, are human experts. They offer personalized advice, can handle complex financial situations, and often build a long-term relationship with you. Both have their perks, and both have their downsides. Let's dive in!

Understanding Robo Advisors The Automated Investment Solution

Robo-advisors are essentially digital platforms that provide automated, algorithm-driven financial planning services with little to no human supervision. They've really taken off because they make investing accessible and affordable for pretty much everyone, especially beginners or those with smaller portfolios. They typically ask you a series of questions about your financial goals, time horizon, and risk tolerance, and then they recommend a diversified portfolio of low-cost ETFs (Exchange Traded Funds) or mutual funds.

Key Features and Benefits of Robo Advisors Accessibility and Cost Efficiency

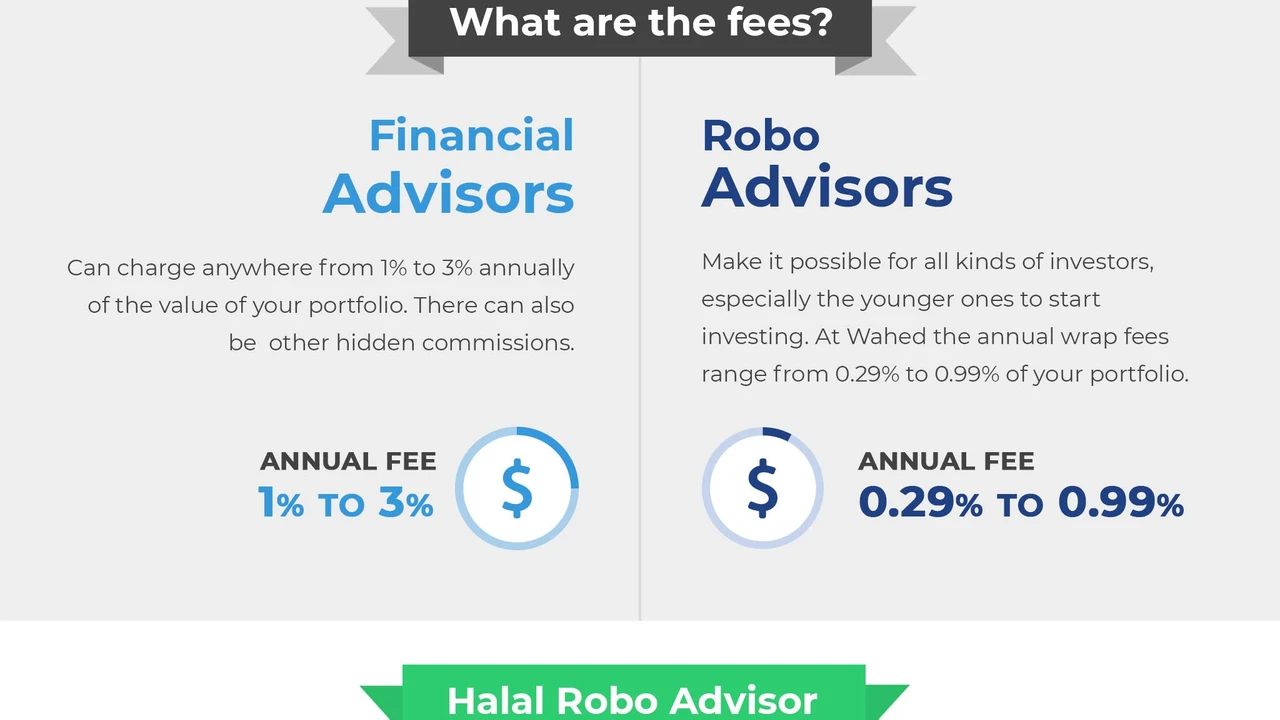

- Lower Fees: This is a huge one. Robo-advisors generally charge a fraction of what traditional advisors do. We're talking about annual fees ranging from 0.25% to 0.50% of assets under management (AUM), compared to 1% or more for human advisors.

- Low Minimums: Many robo-advisors let you start investing with very little money, sometimes as low as $0 or $100. This is fantastic for beginners or those who are just starting to build their wealth.

- Automated Rebalancing: Your portfolio will automatically be rebalanced to maintain your target asset allocation, which is crucial for staying on track with your investment strategy without you lifting a finger.

- Tax-Loss Harvesting: Some advanced robo-advisors offer tax-loss harvesting, which can help reduce your tax bill by selling investments at a loss to offset capital gains.

- Diversification: They typically build globally diversified portfolios using low-cost ETFs, which is a smart way to spread out risk.

- Convenience: You can manage your investments anytime, anywhere, from your phone or computer. Super easy!

Drawbacks of Robo Advisors Limited Personalization and Complex Needs

- Lack of Human Touch: If you prefer talking to a person about your money, robo-advisors might feel a bit impersonal. They can't offer emotional support during market downturns or help you navigate complex life events.

- Limited Scope: While great for investment management, most robo-advisors don't offer comprehensive financial planning for things like estate planning, tax optimization beyond basic harvesting, or complex insurance needs.

- Less Flexibility: The investment strategies are usually pre-set based on algorithms. If you have very specific investment preferences or want to invest in individual stocks, a robo-advisor might not be the best fit.

- Not Ideal for Complex Situations: If you have a high net worth, own a business, or have intricate tax situations, a robo-advisor might not be able to provide the nuanced advice you need.

Popular Robo Advisor Platforms for US and Southeast Asia Markets

Let's look at some specific platforms that are making waves in both the US and Southeast Asian markets. Keep in mind that availability and features can vary slightly by region.

Wealthfront A US Robo Advisor with Advanced Features

- Overview: Wealthfront is a leading robo-advisor in the US, known for its sophisticated features like direct indexing, tax-loss harvesting, and a wide range of investment options. They also offer a high-yield cash account.

- Target Audience: Ideal for investors who want advanced automated features and are comfortable with a hands-off approach.

- Minimum Investment: $500 to start investing.

- Fees: 0.25% annual advisory fee.

- Key Features: Automated tax-loss harvesting, daily rebalancing, direct indexing for accounts over $100,000, and a portfolio line of credit.

- Use Case: A young professional in the US looking to grow their wealth efficiently with minimal effort and benefit from tax optimization.

- Comparison: Offers more advanced tax strategies than some competitors, but has a higher minimum than others.

- Pricing: 0.25% AUM.

Betterment A Comprehensive Robo Advisor for US Investors

- Overview: Betterment is another giant in the US robo-advisor space, offering a user-friendly experience, diversified portfolios, and access to human advisors for an additional fee.

- Target Audience: Great for beginners and those who want a blend of automation and occasional human advice.

- Minimum Investment: $0 to start investing.

- Fees: 0.25% for the Digital plan, 0.40% for the Premium plan (which includes unlimited access to human advisors for accounts over $100,000).

- Key Features: Goal-based investing, automated tax-loss harvesting, rebalancing, and flexible portfolio options.

- Use Case: A couple in the US planning for multiple financial goals like retirement and a down payment, appreciating the option to consult a human advisor when needed.

- Comparison: Offers more human interaction options than Wealthfront at higher tiers, but similar core automated features.

- Pricing: 0.25% - 0.40% AUM.

StashAway A Leading Robo Advisor in Southeast Asia

- Overview: StashAway is a prominent robo-advisor operating across Singapore, Malaysia, Thailand, Hong Kong, and the UAE. They use a proprietary investment framework called ERAA® (Economic Regime-based Asset Allocation) to manage portfolios.

- Target Audience: Investors in Southeast Asia looking for diversified, low-cost investment solutions tailored to their region.

- Minimum Investment: No minimum for general investing.

- Fees: Tiered fees starting from 0.8% for the first S$25,000, decreasing for larger amounts.

- Key Features: ERAA® investment strategy, diversified portfolios of ETFs, goal-based investing, and various portfolio options including thematic portfolios.

- Use Case: A young professional in Singapore looking to invest for their first home or retirement, appreciating the local market focus and diversified approach.

- Comparison: Higher fees than US counterparts but offers localized investment strategies and support for Southeast Asian investors.

- Pricing: Tiered, starting at 0.8% AUM.

Syfe Another Strong Contender in Southeast Asia

- Overview: Syfe is another popular robo-advisor in Singapore and Hong Kong, offering a range of portfolios including diversified core portfolios, thematic portfolios, and even REITs (Real Estate Investment Trusts) portfolios.

- Target Audience: Investors in Southeast Asia seeking diverse portfolio options and competitive fees.

- Minimum Investment: No minimum for most portfolios.

- Fees: Tiered fees starting from 0.65% for the first S$20,000, decreasing for larger amounts.

- Key Features: Diverse portfolio options (Core, REIT+, Equity100, Thematic), automated rebalancing, and fractional share investing.

- Use Case: An investor in Hong Kong interested in gaining exposure to specific sectors like technology or healthcare through thematic portfolios, alongside a core diversified portfolio.

- Comparison: Offers a wider range of specialized portfolios than some other robo-advisors in the region, with competitive fees.

- Pricing: Tiered, starting at 0.65% AUM.

Exploring Traditional Financial Advisors The Human Touch in Finance

Traditional financial advisors are human professionals who provide personalized financial advice and services. They can be fiduciaries (meaning they are legally obligated to act in your best interest) or non-fiduciaries. They typically offer a much broader range of services than robo-advisors, going beyond just investment management.

Key Features and Benefits of Traditional Financial Advisors Comprehensive Guidance and Personalization

- Personalized Advice: This is their biggest selling point. A human advisor can understand your unique financial situation, goals, and even your emotional relationship with money. They can tailor strategies specifically for you.

- Comprehensive Financial Planning: Beyond just investments, they can help with retirement planning, estate planning, tax strategies, insurance needs, college savings, debt management, and more.

- Emotional Support: During volatile market periods, a human advisor can provide reassurance, prevent you from making rash decisions, and help you stick to your long-term plan.

- Complex Situations: If you have a high net worth, own a business, have complex family dynamics, or face unique financial challenges, a traditional advisor can offer the expertise and flexibility needed.

- Relationship Building: Many clients value the long-term relationship they build with an advisor, who becomes a trusted partner in their financial journey.

- Access to Exclusive Investments: Some advisors might have access to certain investment products or strategies not available to the general public or through robo-advisors.

Drawbacks of Traditional Financial Advisors Higher Costs and Potential Conflicts of Interest

- Higher Fees: This is the most significant drawback. Traditional advisors typically charge higher fees, often 1% or more of AUM, or hourly fees, or commissions. These fees can eat into your returns over time.

- Minimum Asset Requirements: Many traditional advisors require a substantial minimum investment, often $100,000, $250,000, or even more, making them inaccessible to new investors.

- Potential for Conflicts of Interest: Not all advisors are fiduciaries. Some may earn commissions on products they sell, which could create a conflict of interest where they recommend products that benefit them more than you. Always ask if they are a fiduciary!

- Time-Consuming: Finding the right advisor can take time, and the initial onboarding process often involves multiple meetings and extensive paperwork.

- Human Bias: While they offer emotional support, advisors are still human and can sometimes be subject to their own biases, though good advisors strive to be objective.

Types of Traditional Financial Advisors Fee Only vs Commission Based

When looking for a traditional advisor, it's crucial to understand how they get paid, as this directly impacts potential conflicts of interest.

Fee Only Advisors The Fiduciary Standard

- How they're paid: They charge a flat fee, an hourly rate, or a percentage of assets under management (AUM). They do NOT earn commissions from selling products.

- Benefit: They are fiduciaries, meaning they are legally and ethically bound to act in your best interest. This minimizes conflicts of interest.

- Use Case: Someone seeking unbiased, comprehensive financial planning and investment advice.

Commission Based Advisors Potential Conflicts

- How they're paid: They earn commissions from selling financial products like mutual funds, annuities, or insurance policies.

- Drawback: There's a potential conflict of interest, as they might be incentivized to recommend products that pay them higher commissions, even if they're not the absolute best fit for you. They are often held to a 'suitability standard' rather than a fiduciary standard.

- Use Case: Less ideal for those seeking purely objective advice, but can be an option if you understand the compensation structure and are comfortable with it.

Hybrid Advisors A Blend of Both

- How they're paid: They may charge a fee for advice and also earn commissions on certain products.

- Consideration: It's important to understand when they are acting as a fiduciary and when they are not. Transparency is key here.

Finding a Traditional Financial Advisor in US and Southeast Asia

Finding a good advisor can be a bit like dating – you need to find the right fit! Here are some resources:

- For US: The National Association of Personal Financial Advisors (NAPFA) and the Certified Financial Planner (CFP) Board websites are great places to find fee-only fiduciaries.

- For Southeast Asia: Look for local financial planning associations (e.g., Financial Planning Association of Singapore, Financial Planning Association of Malaysia) or reputable wealth management firms. Always check their credentials and regulatory status.

Robo Advisors vs Traditional Financial Advisors A Head to Head Comparison

Let's put them side-by-side to make the choice clearer.

Cost and Fees Robo Advisors Win on Affordability

- Robo-Advisors: Typically 0.25% - 0.50% of AUM annually. Some have tiered pricing.

- Traditional Advisors: Often 1% or more of AUM, hourly rates ($100-$300+), or commissions.

- Verdict: If cost is your primary concern, robo-advisors are the clear winner. The difference in fees can amount to tens or even hundreds of thousands of dollars over a lifetime of investing.

Personalization and Complexity Traditional Advisors Excel Here

- Robo-Advisors: Automated, algorithm-driven. Limited personalization beyond risk assessment.

- Traditional Advisors: Highly personalized advice, comprehensive financial planning for complex situations (estate, taxes, business, etc.).

- Verdict: For intricate financial situations, emotional guidance, or a desire for a deep, ongoing relationship, a traditional advisor is superior.

Minimum Investment Requirements Accessibility for All

- Robo-Advisors: Often $0 to $500. Very accessible for new investors.

- Traditional Advisors: Typically $100,000 to $500,000+, making them less accessible for those just starting out.

- Verdict: Robo-advisors open the door to investing for a much wider audience.

Investment Strategy and Product Offerings Diversification and Specificity

- Robo-Advisors: Primarily use low-cost ETFs and mutual funds, focusing on broad market diversification.

- Traditional Advisors: Can offer a wider range of investment products, including individual stocks, bonds, alternative investments, and more tailored strategies.

- Verdict: For standard, diversified portfolios, robo-advisors are excellent. For highly specific or niche investment desires, a traditional advisor might be better.

Convenience and Technology Digital vs Human Interaction

- Robo-Advisors: 24/7 access, easy-to-use apps, automated processes.

- Traditional Advisors: Scheduled meetings, phone calls, more hands-on interaction.

- Verdict: Robo-advisors win on sheer convenience and digital integration.

Who Should Choose a Robo Advisor Ideal Investor Profiles

Robo-advisors are a fantastic fit for several types of investors:

- Beginner Investors: If you're new to investing and want a simple, low-cost way to get started, a robo-advisor is perfect.

- Cost-Conscious Investors: If minimizing fees is a top priority, robo-advisors offer unbeatable value.

- Hands-Off Investors: If you prefer to set it and forget it, and don't want to spend time managing your portfolio, the automation is ideal.

- Investors with Smaller Portfolios: With low or no minimums, robo-advisors make professional investment management accessible to everyone.

- Goal-Oriented Savers: If you have clear goals like retirement or a down payment and want a structured way to save and invest towards them.

- Tech-Savvy Individuals: If you're comfortable with digital platforms and managing your finances online.

Who Should Choose a Traditional Financial Advisor When Human Expertise is Essential

A traditional financial advisor is likely a better choice if:

- You Have Complex Financial Needs: This includes high net worth individuals, business owners, those with complex tax situations, or intricate estate planning requirements.

- You Prefer a Human Connection: If you value personal interaction, emotional support during market volatility, and a trusted advisor to guide you through life's financial ups and downs.

- You Need Comprehensive Financial Planning: Beyond just investments, you need help with budgeting, debt management, insurance, college planning, and more.

- You Have Specific Investment Preferences: If you want to invest in individual stocks, alternative assets, or have very particular ethical investing criteria that require hands-on management.

- You Lack Confidence or Knowledge: If you feel overwhelmed by financial decisions and need someone to explain things clearly and hold your hand through the process.

- You're Approaching or in Retirement: Navigating income streams, healthcare costs, and legacy planning in retirement often benefits from expert human guidance.

Hybrid Approaches Combining the Best of Both Worlds

You don't always have to choose one or the other! Many people find success by combining elements of both:

- Robo-Advisor for Core Investments, Advisor for Specific Needs: Use a robo-advisor for your main, diversified investment portfolio due to its low cost and automation. Then, consult a fee-only financial planner on an hourly or project basis for specific needs like estate planning, tax optimization, or a one-time financial review.

- Robo-Advisor with Human Access: Some robo-advisors (like Betterment Premium) offer access to human advisors for an additional fee. This can be a great middle ground if you want automation but also the option to talk to a professional when needed.

- Gradual Transition: Start with a robo-advisor when your portfolio is smaller and your needs are simpler. As your wealth grows and your financial life becomes more complex, you might then transition to a traditional advisor or a hybrid model.

Making Your Decision Key Considerations for US and Southeast Asian Investors

When making your choice, consider these factors, keeping in mind the nuances of both the US and Southeast Asian markets:

Your Financial Goals and Objectives Long Term vs Short Term

Are you saving for a down payment in two years, or retirement in thirty? Robo-advisors are excellent for long-term, hands-off growth. For very specific, short-term, or complex goals that require intricate planning, a human advisor might be more suitable.

Your Risk Tolerance and Investment Experience Comfort with Volatility

If you're a complete beginner and prone to panic selling during market dips, a human advisor can provide crucial emotional coaching. Robo-advisors are great if you understand your risk tolerance and can stick to your plan without intervention.

Your Budget for Financial Advice Cost vs Value

How much are you willing to pay for advice? If you have a smaller portfolio, the higher fees of a traditional advisor can significantly eat into your returns. For larger, more complex portfolios, the value of comprehensive human advice might outweigh the higher cost.

The Complexity of Your Financial Situation Simple vs Intricate

Do you have a straightforward income and a few investment accounts? A robo-advisor can handle that. Do you own multiple properties, have a trust, or run a business? A traditional advisor is better equipped for such complexity.

Your Preference for Human Interaction or Automation Digital Convenience

Do you prefer clicking buttons on an app or having a face-to-face conversation? Your personal preference for how you interact with your finances is a big factor.

Regulatory Environment and Local Offerings US vs Southeast Asia

In the US, the robo-advisor market is mature with many established players. In Southeast Asia, the market is growing rapidly, with local players like StashAway and Syfe offering tailored solutions. Always check the regulatory status of any platform or advisor you consider in your specific country.

Ultimately, the best choice depends on your individual circumstances. There's no one-size-fits-all answer. Take the time to assess your needs, compare the options, and choose the path that empowers you to achieve your financial dreams. Happy investing!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)