How to Leverage Compounding for Exponential Wealth Growth

Learn how to harness the power of compounding to achieve exponential wealth growth over time in your investments.

Learn how to harness the power of compounding to achieve exponential wealth growth over time in your investments.

How to Leverage Compounding for Exponential Wealth Growth

Hey there, future millionaire! Ever heard the saying, 'Money makes money'? Well, that's essentially the magic of compounding in a nutshell. It's not just some fancy financial jargon; it's a fundamental principle that can turn modest savings into a substantial fortune over time. Whether you're just starting your financial journey or looking to supercharge your existing investments, understanding and actively leveraging compounding is absolutely crucial. Think of it as your money working tirelessly for you, earning returns not just on your initial investment, but also on the returns it has already generated. It's a snowball effect, and once it gets rolling, it can become incredibly powerful. Let's dive deep into how you can make this financial superpower work for you, turning your financial dreams into a tangible reality.

Understanding the Core Concept of Compounding Interest

So, what exactly is compounding interest? In simple terms, it's the interest you earn on both your initial principal and the accumulated interest from previous periods. Unlike simple interest, which is only calculated on the principal amount, compounding allows your earnings to generate their own earnings. This creates an accelerating growth trajectory. Imagine you invest $1,000 at a 10% annual interest rate. After the first year, you'd have $1,100. With simple interest, you'd continue to earn $100 each year. But with compounding, in the second year, you'd earn 10% on $1,100, bringing your total to $1,210. That extra $10 might not seem like much initially, but over decades, those small increments add up to a massive difference. The key ingredients for compounding to truly shine are time, the interest rate, and consistent contributions. The longer your money is invested, the more opportunities it has to compound. A higher interest rate naturally accelerates the process, and regular additions to your principal give the compounding effect more fuel to work with. It's a beautiful cycle of growth that rewards patience and discipline.

The Power of Time Early Investment and Compounding

When it comes to compounding, time is your absolute best friend. The earlier you start investing, the more time your money has to grow exponentially. This is often referred to as the 'eighth wonder of the world' for a reason. Let's look at a classic example: Sarah starts investing $200 a month at age 25, earning an average annual return of 8%. By age 65, she'll have accumulated a significant sum. Now, consider John, who starts investing the same $200 a month at age 35, also earning 8%. Even though John invests for 30 years compared to Sarah's 40, Sarah's final balance will be substantially higher. Why? Because her initial investments had an extra decade to compound. That early start allowed her money to work harder and longer, creating a much larger base for future returns to build upon. This illustrates a critical lesson: don't delay! Even small amounts invested early can outperform larger amounts invested later. The magic isn't just in the amount you invest, but in the duration over which it compounds. So, if you're young, start now. If you're not so young, start today! Every day counts when compounding is at play.

Maximizing Your Compounding Returns Investment Vehicles and Strategies

To truly leverage compounding, you need to choose the right investment vehicles and strategies. Not all investments compound at the same rate or in the same way. Here are some popular options and how they interact with compounding:

Stocks and Equity Funds Long Term Growth Potential

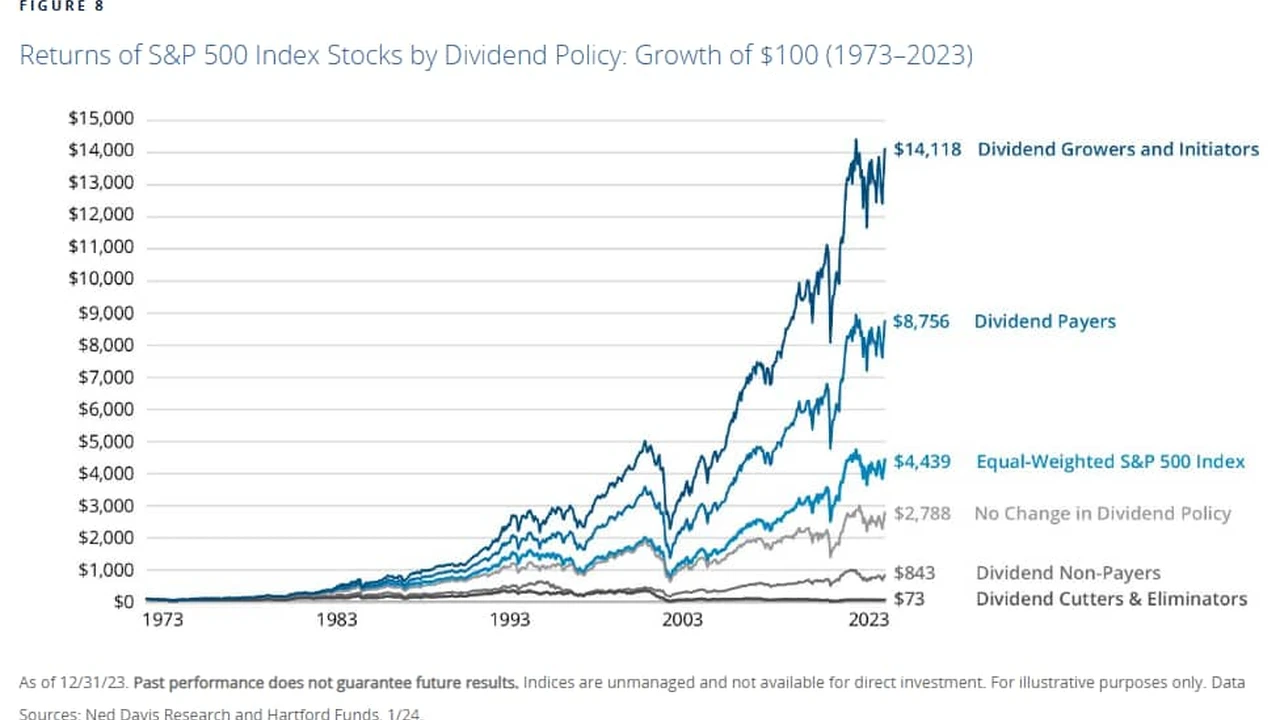

Investing in stocks or equity-focused mutual funds and ETFs is a prime way to harness compounding. When you invest in a company's stock, you're buying a piece of that business. As the company grows and becomes more profitable, its stock price tends to increase. If you reinvest any dividends you receive back into buying more shares, you're directly compounding your returns. Over the long term, the stock market has historically provided some of the highest returns, making it an excellent engine for compounding. For example, if you invest in an S&P 500 index fund, you're essentially investing in the 500 largest US companies, benefiting from their collective growth and reinvesting any dividends. This strategy is often recommended for long-term wealth building due to its historical performance and the power of reinvested dividends.

Retirement Accounts 401k and IRA Tax Advantaged Compounding

Retirement accounts like 401(k)s and IRAs are specifically designed to maximize compounding through tax advantages. Contributions to traditional 401(k)s and IRAs are often tax-deductible, meaning you save on taxes now. Your investments then grow tax-deferred, meaning you don't pay taxes on the gains until retirement. This allows your money to compound without being reduced by annual taxes, leading to significantly larger balances over time. Roth 401(k)s and Roth IRAs offer a different advantage: you contribute after-tax money, but your qualified withdrawals in retirement are completely tax-free. This means all that compounded growth is yours to keep, untouched by the taxman. The tax benefits supercharge the compounding effect, making these accounts indispensable for long-term wealth accumulation. Many employers also offer matching contributions to 401(k)s, which is essentially free money that compounds alongside your own contributions – definitely don't leave that on the table!

Real Estate Investment Properties and REITs

Real estate can also be a powerful compounding asset. When you invest in a rental property, you benefit from rental income, which can be reinvested, and property appreciation. As the property value increases, your equity grows, and you can potentially leverage that equity for further investments. Real Estate Investment Trusts (REITs) offer a more liquid way to invest in real estate. These are companies that own, operate, or finance income-producing real estate. You can buy shares of REITs just like stocks, and they often pay high dividends, which can be reinvested to compound your returns. The combination of rental income, property value appreciation, and potential tax benefits makes real estate a strong contender for compounding wealth, especially over the long haul.

High Yield Savings Accounts and Certificates of Deposit CDs

While not as aggressive as stocks or real estate, high-yield savings accounts (HYSAs) and Certificates of Deposit (CDs) offer a safe way to compound your money, especially for shorter-term goals or your emergency fund. HYSAs offer significantly higher interest rates than traditional savings accounts, and the interest compounds regularly (often monthly). CDs lock in your money for a set period at a fixed interest rate, and the interest compounds over that term. While the returns are lower, they are guaranteed and provide a stable base for compounding. These are great for money you need to keep liquid but still want to grow, or for funds you're saving for a specific goal within a few years. They might not make you rich overnight, but they ensure your money is always working for you, even if at a slower pace.

Practical Tools and Products for Compounding Your Wealth

Now that we've covered the 'why' and 'how' of compounding, let's talk about some specific products and platforms that can help you put these strategies into action. Remember, the best tool is the one you'll actually use consistently!

Robo-Advisors Automated Compounding for Everyone

Robo-advisors are fantastic for beginners or those who prefer a hands-off approach. They use algorithms to manage your investments based on your risk tolerance and financial goals. They automatically rebalance your portfolio and, crucially, often automatically reinvest dividends, supercharging your compounding. They typically have low fees, making them cost-effective for long-term growth.

Product Recommendation 1: Betterment

- Description: Betterment is one of the pioneers in the robo-advisor space, offering automated investing, tax-loss harvesting, and goal-based planning. It invests your money in diversified portfolios of ETFs.

- Use Case: Ideal for hands-off investors, those new to investing, or individuals looking for tax-efficient investing strategies. Great for long-term goals like retirement or a down payment.

- Comparison: Known for its user-friendly interface and robust tax-loss harvesting features. Offers a wider range of account types than some competitors.

- Pricing: 0.25% annual advisory fee for balances under $100,000; 0.40% for balances over $100,000 (Premium plan with human advisor access). Minimum to start is $0 for Digital, $100,000 for Premium.

Product Recommendation 2: Wealthfront

- Description: Wealthfront also offers automated investing with a strong focus on tax optimization, including daily tax-loss harvesting. They provide a wider range of investment options, including a 'Risk Parity' fund and cryptocurrency trusts.

- Use Case: Suitable for investors who want automated management with advanced tax strategies and potentially more diverse investment options, including some exposure to crypto.

- Comparison: Often compared to Betterment, Wealthfront is known for its slightly more aggressive tax-loss harvesting and broader investment offerings.

- Pricing: 0.25% annual advisory fee. Minimum to start is $500.

Brokerage Accounts DIY Compounding

For those who prefer to pick their own investments, a traditional brokerage account is the way to go. You can buy individual stocks, ETFs, mutual funds, and bonds. Many modern brokerages offer commission-free trading, making it easier to reinvest dividends and compound your holdings without incurring extra costs.

Product Recommendation 3: Fidelity

- Description: Fidelity is a full-service brokerage firm offering a vast array of investment products, from individual stocks and bonds to their own low-cost index funds and ETFs. They have excellent research tools and customer service.

- Use Case: Great for both active traders and long-term investors who want a wide selection of investment choices and robust research capabilities. Ideal for building a diversified portfolio and reinvesting dividends manually or automatically.

- Comparison: Known for its extensive investment options, strong research, and competitive pricing on its own funds. Often seen as a top choice for serious long-term investors.

- Pricing: $0 commission for online stock, ETF, and options trades. Many of their own index funds have 0% expense ratios. No account minimum.

Product Recommendation 4: Charles Schwab

- Description: Charles Schwab is another industry giant, offering a comprehensive suite of investment products and services. They are known for their strong customer support, extensive branch network, and competitive pricing.

- Use Case: Similar to Fidelity, Schwab is excellent for investors who want a wide range of choices, good research, and reliable customer service. Their Intelligent Portfolios (robo-advisor) are also popular.

- Comparison: Very similar to Fidelity in terms of offerings and quality. Some investors might prefer Schwab's specific fund offerings or user interface.

- Pricing: $0 commission for online stock, ETF, and options trades. Many of their own index funds have low expense ratios. No account minimum.

Micro-Investing Apps Small Steps Big Compounding

Micro-investing apps allow you to invest small amounts of money regularly, often by rounding up your purchases. This makes investing accessible to everyone and helps build a consistent investing habit, which is crucial for compounding.

Product Recommendation 5: Acorns

- Description: Acorns automatically invests your spare change by rounding up your credit/debit card purchases and investing the difference into diversified portfolios of ETFs. They also offer recurring investments and retirement accounts (Acorns Later).

- Use Case: Perfect for beginners, students, or anyone who struggles to save and invest consistently. It makes investing almost effortless and builds a compounding habit.

- Comparison: Focuses heavily on 'round-ups' and simplicity. While the fees can be high for very small balances, it's effective for getting started.

- Pricing: $3/month for Personal (Invest, Later, Checking); $5/month for Family (Personal + Kids accounts).

Product Recommendation 6: Stash

- Description: Stash allows you to invest in fractional shares of stocks and ETFs, making it possible to invest in expensive companies with small amounts of money. They also offer guided investing and banking features.

- Use Case: Good for beginners who want more control over individual stock picks but still need guidance. It helps demystify investing by allowing you to invest in companies you know and understand.

- Comparison: Offers more direct stock picking than Acorns, but still with a guided approach. Focuses on themed investments.

- Pricing: $3/month for Growth (Invest, Banking, Retirement); $9/month for Plus (Growth + Kids accounts, higher life insurance).

Digital Banks and Investment Platforms in Southeast Asia

For our friends in Southeast Asia, the landscape is rapidly evolving with many digital banks and investment platforms emerging, offering competitive rates and easy access to investing.

Product Recommendation 7: Syfe (Singapore)

- Description: Syfe is a digital investment platform (robo-advisor) in Singapore offering diversified portfolios of ETFs, including core portfolios, REITs, and thematic investments. They focus on low fees and automated investing.

- Use Case: Excellent for Singapore-based investors looking for automated, diversified portfolios with low fees. Good for long-term wealth building and specific financial goals.

- Comparison: Similar to Betterment/Wealthfront but tailored for the Singapore market. Offers a wider range of portfolio options than some local competitors.

- Pricing: 0.35% - 0.65% annual management fee, depending on the invested amount. No minimum investment.

Product Recommendation 8: GrabInvest (Southeast Asia)

- Description: GrabInvest, part of the Grab ecosystem, offers micro-investing solutions like 'AutoInvest' where you can invest small amounts from your GrabPay wallet into low-cost funds. Available in Singapore and Malaysia.

- Use Case: Ideal for Grab users who want to start investing with very small amounts and integrate it into their daily spending habits. Great for building an investing habit.

- Comparison: Leverages the existing Grab user base for easy access to investing. Focuses on simplicity and accessibility for micro-investments.

- Pricing: Low management fees, typically around 0.45% - 0.65% per annum, depending on the fund. Very low minimum investment.

Strategies to Accelerate Your Compounding Journey

Beyond choosing the right tools, certain strategies can significantly boost your compounding returns.

Consistent Contributions The Fuel for Compounding

Regularly adding money to your investments is like adding fuel to a fire. The more you contribute, the larger your principal becomes, and the more money you have to compound. Even small, consistent contributions can make a huge difference over time. Set up automatic transfers from your checking account to your investment account. This 'set it and forget it' approach ensures you're always contributing, even when life gets busy. Whether it's $50, $200, or $1,000 a month, consistency is key. This discipline helps you overcome market fluctuations because you're buying at different price points, a strategy known as dollar-cost averaging, which itself is a powerful way to enhance long-term compounding.

Reinvesting Dividends and Capital Gains

This is a critical component of compounding. When your investments pay dividends or generate capital gains, resist the urge to take that money out. Instead, reinvest it back into the same investment or another one. This means you're buying more shares, and those new shares will then generate their own dividends and capital gains, creating a powerful feedback loop. Many brokerage accounts and robo-advisors offer automatic dividend reinvestment plans (DRIPs), making this process seamless. This simple act of reinvestment can dramatically increase your total returns over the long run, as your money is constantly working to create more money.

Minimizing Fees and Taxes The Silent Killers of Compounding

Fees and taxes are like tiny termites eating away at your compounded returns. Even seemingly small fees, like a 1% annual expense ratio on a mutual fund, can cost you tens or even hundreds of thousands of dollars over several decades. Choose low-cost index funds and ETFs over actively managed funds with high expense ratios. Utilize tax-advantaged accounts like 401(k)s, IRAs, and Roth IRAs to allow your investments to grow tax-deferred or tax-free. In taxable accounts, employ strategies like tax-loss harvesting (offered by some robo-advisors) to offset gains. Every dollar saved on fees and taxes is a dollar that can continue to compound for you.

Patience and Long Term Perspective The Ultimate Compounding Hack

Compounding is not a get-rich-quick scheme. It's a get-rich-slowly-but-surely strategy. The biggest gains from compounding come in the later years of your investment journey. This requires patience and a long-term perspective. Don't panic during market downturns; in fact, these can be opportunities to buy more assets at a lower price, which will then compound even more aggressively when the market recovers. Resist the urge to constantly check your portfolio or make impulsive decisions based on short-term market noise. Trust the process, stay invested, and let time do its magnificent work. The longer you allow your money to compound, the more astonishing the results will be.

Common Pitfalls to Avoid When Compounding

While compounding is powerful, there are common mistakes that can hinder its effectiveness. Being aware of these can help you stay on track.

Starting Too Late The Missed Opportunity

As we discussed, time is the most crucial factor. Delaying your investments, even by a few years, can cost you a significant amount of potential compounded growth. The 'future you' will thank the 'present you' for starting early. Don't wait for the 'perfect' time or for a large sum of money to get started. Begin with what you can, and build from there.

Frequent Withdrawals Interrupting the Snowball

Every time you withdraw money from your investment account, you're essentially taking a chunk out of your compounding snowball. This reduces the principal amount that can generate future returns, slowing down your growth. Try to avoid dipping into your investments unless absolutely necessary, especially for long-term goals like retirement. Keep your emergency fund separate to avoid this temptation.

Chasing High Returns and Market Timing

While a higher interest rate accelerates compounding, chasing excessively high returns often comes with significantly higher risk. Trying to time the market (buying low and selling high) is notoriously difficult and often leads to worse returns than a consistent, long-term approach. Focus on diversified investments with reasonable, consistent returns rather than speculative ventures. Slow and steady wins the compounding race.

Ignoring Inflation The Silent Wealth Eroder

Inflation reduces the purchasing power of your money over time. If your investments are only earning 2% and inflation is 3%, you're actually losing purchasing power. Ensure your investments are generating returns that outpace inflation to ensure your wealth is truly growing in real terms. This is why simply keeping money in a low-interest savings account isn't enough for long-term wealth building.

The Compounding Mindset Cultivating Financial Discipline

Ultimately, leveraging compounding for exponential wealth growth isn't just about understanding the math; it's about cultivating a specific mindset. It requires discipline, patience, and a long-term vision. It means prioritizing saving and investing today for a more prosperous tomorrow. It means resisting instant gratification and embracing the power of delayed gratification. When you adopt a compounding mindset, you start to see every dollar saved and invested not just as a dollar, but as a seed that can grow into a tree, and then a forest, over time. It's a powerful shift in perspective that can transform your financial life. So, start planting those seeds today, nurture them with consistent contributions and smart choices, and watch your financial forest grow exponentially.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)